BOSTON, Massachusetts – The golf industry has reason to celebrate with America marking 250 years since the Declaration of Independence, golf has its own long-established place in the country’s sporting and leisure landscape.

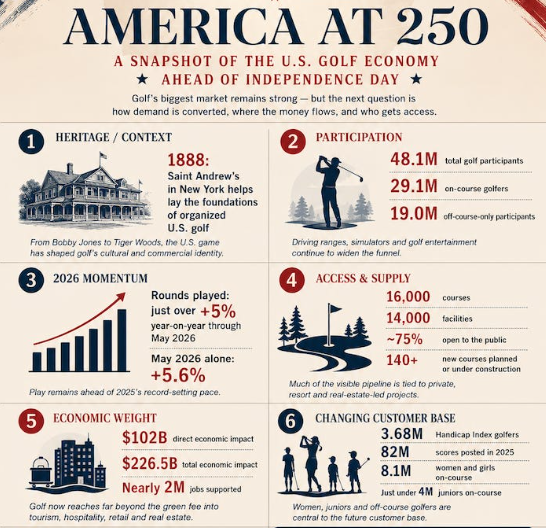

The American game is traced back to the late 19th century to The Country Club in Brookline (MA) and the origins of the United States Golf Association originally formed in 1894 to resolve the question of a national amateur championship. About that time, the Newport Country Club and Saint Andrew’s Golf in New York helped lay the foundations for what became the world’s largest golf market. From Bobby Jones and Ben Hogan to Arnold Palmer, Jack Nicklaus, and Tiger Woods, the US game has since shaped golf’s competitive, cultural, and commercial identity.

That history matters because the current US golf market did not appear suddenly. It has moved through club formation, public-course growth, television expansion, the Tiger Woods effect, overbuild and correction, and a post-pandemic surge.

According to the National Golf Foundation the numbers remain strong. The latest industry data puts total US golf participation at 48.1 million people aged six and above, including 29.1 million on-course golfers and 19 million who participated only through off-course formats such as driving ranges, indoor simulators, and golf-entertainment venues.

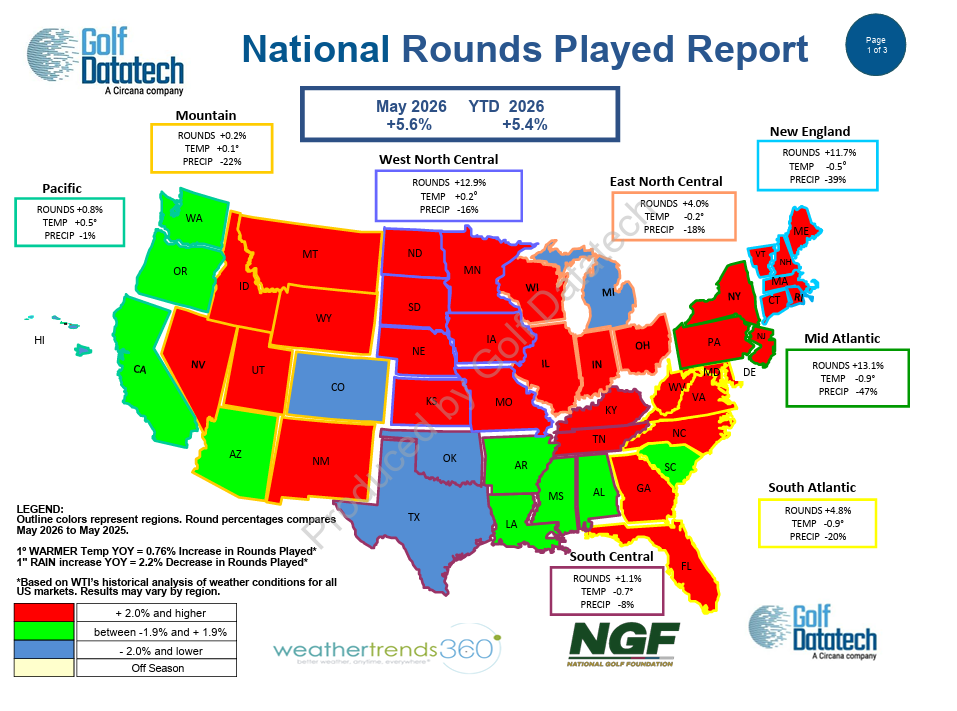

The momentum has carried into this year. Through May 2026, US rounds were tracking just over 5% ahead of last year’s record-setting pace, with May itself up 5.6% year-on-year. The USGA’s 2025 Golf Scorecard also reported that 3.68 million golfers with a Handicap Index posted a record 82 million scores domestically last year.

The current US golf market is not simply a replay of the Tiger-era boom.

The US remains well served by golf infrastructure, with approximately 16,000 courses at 14,000 facilities at the end of 2025 and about three-quarters open to the public. But access is not evenly distributed, and municipal golf remains important because it is often where participation starts.

New course development has returned, but much of the visible pipeline is weighted towards a different part of the market. At the start of 2026, more than 140 new courses were in planning or under construction, with the majority tied to private destination clubs, high-end real estate communities, and resort properties.

The economic footprint explains why capital is interested. The American Golf Industry Coalition says golf has a direct economic impact of $102 billion in the United States and a total impact, including indirect and induced activity, of $226.5 billion. It also says the industry supports nearly two million jobs nationally.

Golf is now tied to employment, tourism, hospitality, retail, real estate, media, charity, and local tax bases. In a destination market, a round becomes part of wider spend across hotels, restaurants, transport, retail, property, and hospitality.

But the future of US golf will not be decided only by affluent travelers and premium venues. The larger question is conversion.

The 19 million off-course-only participants are one of the most important groups in the American golf economy. They show that interest is being created beyond the traditional course. The challenge is whether that interest can become coaching, equipment purchases, green-grass rounds, memberships, golf trips, or other repeat spending.

Some may never want traditional 18-hole golf. That is not necessarily a problem. It means the industry needs a more flexible view of what a golf customer now looks like.

The demographic picture reinforces that point. Industry data shows just under four million juniors played on course in 2025, the highest figure since 2004, while female on-course participation reached 8.1 million. Women now represent 28% of on-course golfers, 35% of beginners, 35% of juniors, and 43% of off-course-only participants.

The professional game adds another layer. PGA Tour Enterprises has pushed the Tour further towards a sports-property model built around capital, player equity, media value, and premium competition.

American golf is in a strong position. Participation is high. Rounds remain elevated. Women and juniors are changing the market. Off-course formats are widening the funnel. New course development is returning.

The current task is to keep new golfers in the game, serve them better, and convert broader interest into sustainable economic value.

As America marks 250 years since independence, the question is no longer whether golf can attract attention. In the US, it clearly can. The more important question is who gets access, who captures the money, and whether the current strength of the American game becomes a broader platform for sustainable growth or a more limited premium cycle.

{kind=link}